How to Teach Kids About Money: A Dad’s Simple Guide

Let's be honest—talking about money with our kids can feel… awkward. Maybe it’s because no one really talked about it with us growing up, or we worry we don’t have all the answers ourselves. But you don't need to be a financial wizard to give your kids a massive head start.

The real goal is to strip away the mystery and make money a normal, everyday topic. It's not about complex lectures on the economy. It’s about weaving simple financial truths into daily life, turning a subject that’s often taboo into a practical tool for building a good life.

When you start these conversations early, you’re doing more than just teaching them to count coins. You're laying the groundwork for a healthy, confident relationship with their finances that will serve them for decades.

Why Talking About Money Early Changes Everything

The sooner you start, the better. Making money a regular part of your conversations demystifies it and dials down the anxiety that so many adults feel around the subject. You’re preventing it from ever becoming a scary or forbidden topic.

The data backs this up. The FINRA Foundation's National Financial Capability Study found that adults who received financial education as kids were far more likely to save regularly. They were also less likely to be drowning in credit card debt. The positive effects are crystal clear.

The point isn’t to raise a mini-accountant. It's to raise a child who sees money for what it is: a resource to achieve their goals, help others, and live a life full of choice and responsibility.

The lessons you pass on are about so much more than dollars and cents. You’re instilling patience, foresight, and personal responsibility. Frankly, these are some of the most crucial things every dad should teach his kids, forming the bedrock of a successful life.

How to Start the Conversation (Without Making It Weird)

So, where do you begin? Right where you are. Just start involving your kids in the small financial moments of your day.

Let them see you pay for groceries. Talk out loud about why you might grab the store brand cereal instead of the pricier one. When you use the ATM, explain that it’s not spitting out free cash—it’s taking money you already earned from your bank account.

These little interactions make abstract concepts real. They connect the dots for young minds in a way no lecture ever could.

To help you get the ball rolling, here's a simple breakdown of the core ideas and some easy, dad-friendly activities to try.

Your First Money Conversations

This table breaks down the three core money concepts to help you start talking with your child today. These simple definitions and starter activities are designed to be hands-on and easy to integrate into your routine.

| Concept | Simple Definition for Kids | Starter Activity for Dads |

|---|---|---|

| Earning | Money you get for doing work. | Set up a "job chart" for extra chores beyond their normal duties, like helping wash the car or rake leaves for a small commission. |

| Saving | Keeping money to use later for something special. | Get a clear jar for savings. This lets them see their money grow as they work toward a specific goal, like a new toy or book. |

| Spending | Using money to buy things you need or want. | On your next store run, give them a small amount ($2-$3) to make their own choice, like picking out a piece of fruit or a small treat. |

By using simple activities like these, you’re not just telling them about money—you're letting them experience it firsthand. And that hands-on approach is what makes the lessons stick, building a foundation of financial confidence one small, meaningful conversation at a time.

Making Money Real for Preschoolers

For a three or four-year-old, money is basically magic. It’s the colorful paper or shiny circles you hand over to get a toy or a snack. The idea that it's a limited resource you have to earn is a completely foreign concept.

Our job as dads is to take that abstract idea and make it real. We have to make it tangible, visual, and even a little fun. This is where you start when teaching kids about money, right at the beginning of their journey to understand the world.

At this age (3-5 years old), you have to think in physical, hands-on terms. Forget spreadsheets or digital trackers. The single most effective tool I've found is the classic "Three Jars" system.

Grab three clear containers—mason jars are perfect because your kid can literally watch their money grow. Label them: Save, Spend, and Share.

Whenever your child gets some money, maybe from a birthday or as a small reward, you sit with them and help them divide it among the jars. This simple ritual introduces three massive financial ideas in a way their little minds can actually grasp. It's not just about getting money; it's about making a plan for it.

Turning Chores into Earning Opportunities

The connection between work and money is a cornerstone of financial literacy. For preschoolers, this doesn't need to be some rigid system where every little thing has a price tag. Instead, you introduce the idea of "extra jobs" that go beyond their normal family duties, like putting their own toys away.

You can break it down like this:

- Family Chores (Unpaid): These are just part of being in the family. Think helping set the table or tossing their dirty clothes in the hamper.

- Earning Jobs (Paid): These are specific tasks with a clear start and finish. This could be helping you wash the car, pulling weeds for ten minutes, or carrying in a few light grocery bags.

The key is making the payment small and immediate. Handing them a few coins right after they’ve helped you wipe down the patio table creates a powerful, instant connection. They did something, and now they have something tangible to show for it—money to put in their jars.

This isn't about creating a tiny employee. It's about teaching them that effort creates value. That pride they feel when they drop a hard-earned quarter into their "Spend" jar is a lesson that will stick with them for life.

The Power of Physical Cash

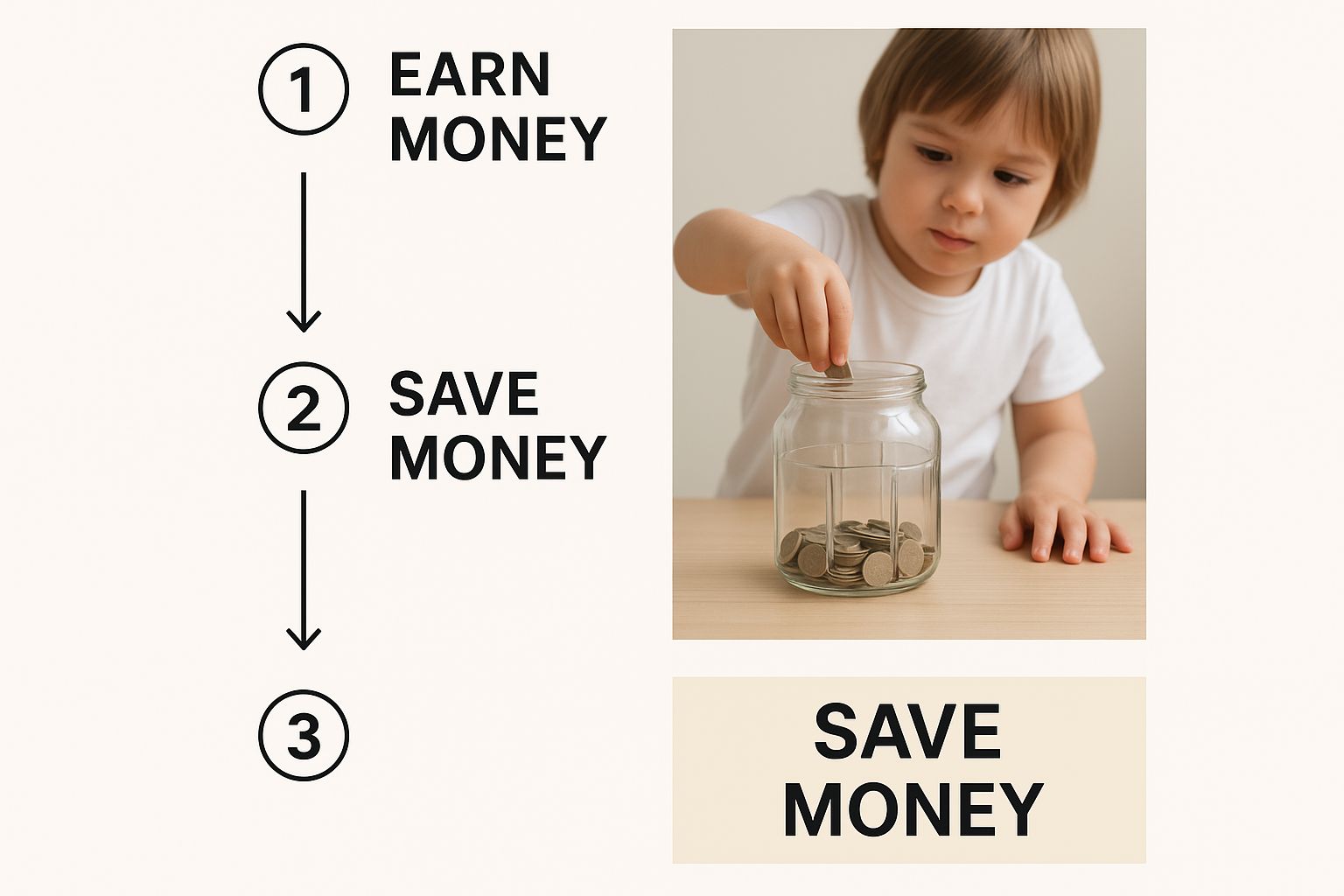

In a world of tapping cards and digital payments, using physical money with preschoolers is non-negotiable. They need to see, touch, and count the actual coins and bills. This sensory experience is what makes the concept of value real.

A study on early childhood cognition backs this up, showing that kids under five learn best through concrete, hands-on experiences. A number on a screen just doesn't mean anything to them. That visual process of dividing real coins is a fundamental first step in teaching kids to save.

This image of a child putting money into a jar perfectly captures it—a simple, powerful act of choosing to save for the future.

Practical Lessons at the Grocery Store

Your weekly trip to the grocery store is the perfect real-world classroom. Instead of just trying to survive it, turn it into a money adventure. Give your child a small, specific mission.

For example, say, "We need to buy crackers. The red box costs $3, and the blue box costs $4. Which one should we get if we want to save some money?" This simple question introduces huge concepts like price comparison and value.

Another great move is to let them handle a transaction. If you're buying a single item like a banana, let them hold the money and physically hand it to the cashier. Let them get the change back. This small act of participation is incredibly empowering and reinforces the core idea that money is exchanged for goods. These are the kinds of essential life skills for children that build real confidence and practical know-how from a young age.

By using these simple, interactive strategies, you're not just showing them what money is. You're building a healthy, positive foundation for their entire financial future, one coin and one choice at a time.

Getting Real About Earning and Saving in Elementary School

Once your kids hit elementary school, their world starts to get a lot bigger. Suddenly, those little sponges who were just playing with coins can now connect the dots between effort and reward. This is your cue, Dad. It's time to shift the conversation from simply having money to understanding where it comes from.

The 6-to-10-year-old brain is primed for this stuff. They get fairness, they can handle basic math, and they've developed enough patience to work for a goal that isn't five minutes away. Your job is to create a simple framework that makes these lessons stick.

Allowance vs. Commissions: Picking Your Play

One of the first forks in the road you'll hit is how your kids actually get money in their hands. It usually comes down to two main camps: a straight-up allowance or a commission-based system tied to chores. There's no magic bullet here—what works best really depends on your family's philosophy.

Let's break them down.

- Straight Allowance: This is a fixed amount of cash, paid out regularly (usually weekly), no strings attached. The argument here is that it teaches kids how to budget a predictable income. Plus, many parents feel that chores are just part of being in a family, not a paid gig.

- Chore-Based Commissions: In this model, money is earned by completing specific jobs. It's a direct, undeniable lesson in the work-for-pay principle. Don't do the job, don't get the cash. Simple.

A lot of dads I know land on a hybrid model. Kids have their non-negotiable family duties (making the bed, clearing their own plate). Then, there's a separate "jobs board" with extra tasks they can tackle for cash, like washing the car or pulling weeds. This approach teaches both family contribution and the value of hustling for extra money.

Helping Them Set That First Big Savings Goal

This is the age where the power of delayed gratification really starts to click. That old three-jar system (Save, Spend, Share) is still a winner, but now the "Save" jar gets a real mission. It's no longer just saving for the sake of it; it’s saving for something they actually want.

This is your coaching moment. Sit down with your kid and find out what they’re dreaming about. That new LEGO set? A video game they can't stop talking about? The scooter they point out every time you pass the park?

Once you have a target, you can help them map out the journey:

- Nail Down the Price: Jump online and look it up together. Let's say that LEGO set is $40.

- Do the Simple Math: If they can earn $5 a week, help them figure out how long it will take. ($40 divided by $5 is 8 weeks).

- Track the Progress: This is the fun part. Grab a piece of paper and make a simple chart for the fridge. Every week they drop money into their "Save" jar, they get to color in another square.

That visual tracker is a game-changer. It makes an abstract idea like "eight weeks" feel real and exciting. They can literally see their hard work paying off.

That moment when your kid finally marches into the store with a jar full of their own money to buy that LEGO set? It’s pure gold. You'll see a look of pride on their face that no lecture from you could ever replicate. That experience is the real teacher.

Why Your Lessons at Home Matter So Much

The money talks you have around the kitchen table are more critical than you might think. We'd all love for schools to handle this, but the truth is, not every kid has access to a great education, let alone financial literacy classes.

The UNESCO Global Education Monitoring Report paints a stark picture, showing that millions of children worldwide are out of school, completely missing the chance to learn about money in a formal setting. This just hammers home the impact a dad can have.

You're filling a massive gap. By setting up these simple earning and saving systems, you're giving your kids a hands-on education in financial responsibility. You’re teaching them to be producers, not just consumers. That mental shift is a foundation for a life of confidence and financial well-being.

Navigating Wants, Needs, and First Jobs with Teens

The teenage years are where your money lessons really hit the real world. The stakes get higher, the goals get bigger, and their financial world suddenly becomes way more complex than just filling a piggy bank.

This is where your role shifts. You move from being the coach on the sidelines to a trusted advisor, helping them navigate some of their first major financial milestones. The conversations change from simple saving goals to dissecting wants versus needs, understanding the subtle power of advertising, and making smarter choices. It's no longer about a toy—it's about concert tickets, a phone, or even their first car.

Distinguishing Wants from Needs

That line between a "want" and a "need" gets incredibly blurry for a teenager, especially when they're bombarded with social media trends and peer pressure. A new pair of sneakers can absolutely feel like a critical need. This is the perfect time to help them build some perspective.

The trick is to make it a collaborative exercise, not a lecture. The next time they come to you wanting an expensive item, grab a piece of paper and draw two columns: Wants and Needs. Talk it through together.

- Needs: Food, basic clothes, shelter, school supplies. These are the non-negotiables.

- Wants: The latest iPhone, designer labels, daily coffee runs, streaming subscriptions.

This simple visual helps them start categorizing their own desires. It’s not about denying them their wants, but about teaching them how to prioritize and plan for them. The real goal is for them to eventually ask themselves, "Do I truly need this, or do I just want it?"

The First Job and the First Paycheck

Getting their first job is a massive step. It’s a huge dose of independence. But the real lesson begins when that first paycheck lands. It’s almost always smaller than they expected, and that moment of confusion is a golden teaching opportunity.

Sit down with them and go through the pay stub. Explain what each deduction means in simple, real-world terms.

- Federal/State Taxes: "This is money that helps pay for things we all use, like roads, parks, and schools."

- FICA (Social Security/Medicare): "Think of this as a savings plan for when people get older or need help with medical care."

This simple conversation transforms taxes from some frustrating mystery into a concrete concept. It’s their first real-world lesson in how income actually works.

When your teen sees their gross pay shrink down to their net pay, it’s often a shock. Frame this not as a loss, but as their first real look at how personal finance works. It's a fundamental lesson that the money you earn isn't the same as the money that hits your pocket.

Opening Their First Bank Account

With a job comes the need for a place to put their money. It's time to graduate from the savings jar to a real bank account. Helping them open their first student checking and savings account is a rite of passage.

Go with them to the bank, but let them lead the conversation with the banker as much as possible. This simple act demystifies the whole banking system and builds their confidence. Once the account is open, teach them the basics.

- Using a debit card: Hammer this home: it’s not a magic card for free money. The funds come directly out of their account, right now.

- The danger of overdraft fees: Explain how spending more than they have results in expensive penalties.

- Checking their balance: Show them how to use the mobile banking app to track their money in real time.

This is where they can make small, low-stakes mistakes under your guidance. That’s far better than them learning these lessons the hard way, with bigger consequences, later on.

The need for this kind of practical education is staggering. The World Bank warns the recent global learning crisis could cost the current generation of youth US$21 trillion in lifetime earnings. Globally, almost 25% of young adults aren't in employment, education, or training, a problem made worse by a lack of financial skills. You can learn more about the link between education and economic potential and see how the World Bank is addressing these challenges.

Introducing Big-Picture Concepts

Once they have a steady income and a bank account, you can start introducing more advanced, long-term ideas. The key is to connect these big concepts directly to their own goals.

If they're saving for a car, it's the perfect time to talk about compound interest. Use an online calculator to show them how even small, regular savings can grow into something much bigger over time. This transforms saving from a boring chore into an exciting game.

On the flip side, use this chance to explain the dangers of debt. Talk about how credit card interest works in reverse, making everything more expensive. Relate it to their world: "Imagine paying $40 for that $25 video game because of interest. Is it still a good deal?"

By grounding these big ideas in their immediate goals and experiences, you make financial education stick. You’re not just teaching your teen how to manage a few bucks; you're giving them the critical thinking skills to build a secure and independent future.

The Money Mistakes We All Make (And How to Dodge Them)

Look, we all want to get this right. We have the best intentions when we start teaching our kids about money. But even so, it's surprisingly easy to trip over our own feet and accidentally send the wrong signals.

The biggest pitfall? Sending mixed messages. You can preach about saving all week, but if you then make a big, impulsive purchase right in front of them without a word of explanation, your actions just drowned out your lesson. Kids notice these contradictions, and it waters down everything you're trying to teach.

Another classic mistake is only talking about money when you’re stressed out. If the only time your kids hear about finances is during a tense conversation about bills, they'll start to connect money with anxiety. It becomes a source of fear instead of a tool for building a good life.

The Problem with Being the Rescue Squad

It’s a dad's instinct to shield our kids from disappointment. When they blow their allowance on a cheap toy that breaks in five minutes and then have zero cash for the movie they wanted to see, our gut tells us to bail them out.

While this comes from a place of love, constantly saving them from their financial blunders robs them of a powerful teacher: natural consequences. A little buyer’s remorse at age nine is a cheap lesson. It can prevent some seriously expensive pain at age twenty-nine.

Try This Instead: Let them feel the sting of a bad choice. When the money’s gone, it’s gone. Use it as a teachable moment, not an "I told you so." Calmly ask, "What do you think you’ll do differently next time?" This simple question turns a mistake into a memorable lesson in budgeting.

Using Guilt or Punishment for Money Missteps

When your teenager torches their first paycheck in a single weekend, it’s tough not to get frustrated. The "I told you so" lecture is right there on the tip of your tongue, along with the urge to tighten the leash.

But that approach almost always backfires. It wraps their financial mistake in a layer of shame, making them less likely to come to you for advice in the future. They learn to hide their money life from you instead of seeking your guidance.

What to Do Instead of Punishing:

- Focus on the next play: Frame the chat around their next paycheck. "Okay, that didn't go how you planned. Let's make a simple game plan for the next one so you have money left for the things you really want."

- Share your own fouls: Be real about a time you blew it with money. It makes you relatable and shows that everyone messes up. It's a huge part of being a better dad and builds trust.

- Figure out the 'why': Talk about what drove the spending spree. Was it peer pressure? An impulse buy? Getting to the root cause is way more productive than just slamming the outcome.

Our goal isn’t to raise a perfect accountant overnight. It's to open up an honest conversation where mistakes are seen as learning opportunities, not failures. By steering clear of these common traps, you’ll help your kids build a healthier, more resilient attitude toward money—setting them up for a lifetime of smarter choices.

Your Questions on Kids and Money Answered

Even with the best game plan, you’re going to hit some tricky spots when teaching your kids about money. This is where the real coaching happens—in those messy, real-world moments. Here are the most common questions I hear from other dads, with straightforward answers for those tough, in-the-moment decisions.

At What Age Should I Start Giving My Child an Allowance?

There's no magic number here, but many dads find the sweet spot is around 5 or 6 years old. By then, most kids can handle basic addition and really get the idea of trading money for something they want.

Honestly, the exact age is less important than the routine. You're trying to build a habit. Link the allowance to a few simple responsibilities they can actually manage, start small, and focus on the rhythm of earning, saving, and spending.

Should Allowance Be Tied to Chores?

Ah, the classic debate. You'll hear strong arguments on both sides, and both have merit.

Tying allowance to specific, “above-and-beyond” chores makes the work-for-pay connection crystal clear. Wash the car, get paid. Don't wash the car, don't get paid. Simple.

On the other hand, some things just need to be done because you're part of the family—like making your bed or clearing your plate. A hybrid approach usually works best.

- Family Contributions (Unpaid): These are the daily tasks that keep the household running.

- Paid "Jobs" (Optional): These are extra chores they can choose to do for cash, like raking leaves or helping you with a weekend project.

This way, they learn about both family responsibility and the value of putting in extra effort to earn money.

Let your child experience the natural consequences of a bad purchase. Resist the urge to bail them out. That feeling of buyer's remorse over a cheap, broken toy is a powerful, low-stakes lesson in budgeting and opportunity cost.

How Do I Handle My Kid Constantly Losing Their Money?

This one is frustrating, I get it. Your first instinct is probably to just replace the lost five-dollar bill to avoid a meltdown. Don't.

Instead, use it as a teaching moment. Calmly talk through the direct consequence: "Well, since the money is lost, you won't be able to buy that LEGO set you were saving for this week." It stings, but that feeling is what makes the lesson stick.

This is their first real taste of responsibility. Help them problem-solve for next time. Get them a specific wallet or a special "money box" for their room so they have a designated safe spot.

What if My Teenager Makes a Bad Spending Decision?

Your teen just blew their entire paycheck on a new video game and now can't afford movie tickets with their friends. Whatever you do, resist the "I told you so."

Let them feel the full weight of that choice. This is where abstract ideas like budgeting and opportunity cost become painfully real. When they're sitting at home on a Friday night, the lesson is hitting home harder than any lecture you could give.

Later, when things are calm, you can have a productive chat. Frame it as a strategy session, not a critique. "Okay, that didn't go as planned. What could we do differently with your next paycheck to make sure you have money for the things you want to do?"

At Vibrant Dad, we believe building a strong family means teaching the practical life skills that matter. For more strategies on optimizing your life and being a more present father, explore our resources at https://vibrantdad.com.